Things are starting to get a little more exciting. The remaining balance totals are smaller and the light at the end of the tunnel brighter.

Currently sitting at 74.6% payoff completed. 0% balances due to be gone mid October. 4 digit student loan balance the only thing left after that.

I'll be honest, I'm not completely sure whether I'll aggressively pay off the student loans or aggressively add to savings. In the month of July I opened up a Traditonal IRA to go with my Roth IRA. I've started a small monthly deposit into that, which provides another tax deferring account to go along with my 401k and HSA. It also provides a landing spot to roll over that 401k eventually. Win.

My thought is for the remaining 2 1/2 months of the year, max out my HSA and traditional IRA to lower my taxable income for 2019. Then pay off the student loans early next year. I see more of a benefit in doing that. The increased tax return would go directly to the student loans.

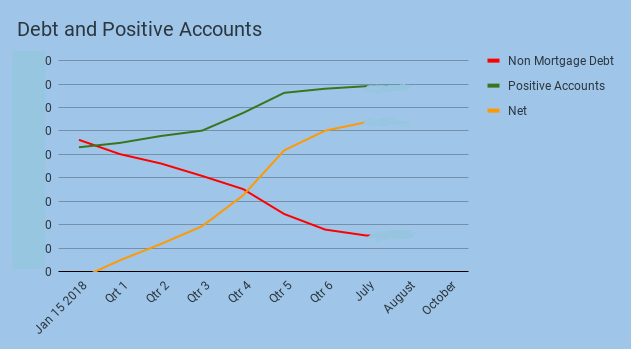

The graph:

Let's keep it rolling.

Minimal fitness - weight is still down, haven't been caring about tallying miles as closely lately. Not running, more cycling/body weight workouts. Headed back out on the AT in the near future to get in just under 40 miles on the trail.

Comments

Post a Comment