I have a terrible long term memory. When I say terrible, I mean, it's horrendous. I've reflected a bit on this recently, and I think my natural level of anxiety (or the anxiety I developed in my childhood) always has me thinking in the future. I rarely think about the past, if ever. My headspace is always consumed with the tomorrows that have yet to happen. This isn't healthy, and I've really been working on staying mindful and present, but...

...it makes me more goal oriented than most, and this is probably to a fault. My daily choices and abilities are often packaged with thoughts that I can do/achieve better, at the expense of thinking positively about what I've been able to achieve. When I latch on to a goal and actually stay with it, though, it focuses my thoughts and can reduce overall anxiety.

This financial goal has done just that. It's given me a focal point, and it's given me a positive mindset to base my decisions on.

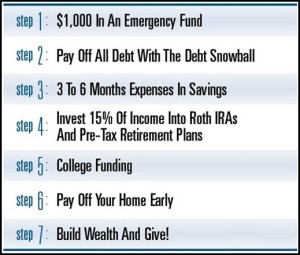

I sat through another benefits seminar yesterday, and the retirement/401k presentation had me daydreaming about the future. When I set out on this journey, I had Dave Ramsey's basic tenets in mind:

I was thinking about step 2 and 4. The presentation had me excited about the potential of reaching the point where I can begin funding my 401k and Roth at max levels allowed. I began to wonder if I should be doing this before I fully complete step 2. There are certain debts I definitely want gone - credit cards, personal loan, and car. When considering my student loans, however, I started thinking that as soon as that's the only debt left, I move on to steps 3 and 4.

Here is my reasoning. My student loan interest rate is at 4.5%. That interest paid is also deducted on my taxes. The power of growth within my 401k and Roth is worth taking advantage of, and the earlier you do it the more powerful it is. Let's say the compounding growth is an average of 6%. My money is accomplishing more going into those accounts, than it is paying off those student loans (gaining 6% instead of losing 4.5%). I'd obviously try to pay this off as quick as possible, but I think funding both retirement accounts at their max potential is more important.

Thoughts? Let me know if you have an opinion.

Happy Hump Day.

...it makes me more goal oriented than most, and this is probably to a fault. My daily choices and abilities are often packaged with thoughts that I can do/achieve better, at the expense of thinking positively about what I've been able to achieve. When I latch on to a goal and actually stay with it, though, it focuses my thoughts and can reduce overall anxiety.

This financial goal has done just that. It's given me a focal point, and it's given me a positive mindset to base my decisions on.

I sat through another benefits seminar yesterday, and the retirement/401k presentation had me daydreaming about the future. When I set out on this journey, I had Dave Ramsey's basic tenets in mind:

I was thinking about step 2 and 4. The presentation had me excited about the potential of reaching the point where I can begin funding my 401k and Roth at max levels allowed. I began to wonder if I should be doing this before I fully complete step 2. There are certain debts I definitely want gone - credit cards, personal loan, and car. When considering my student loans, however, I started thinking that as soon as that's the only debt left, I move on to steps 3 and 4.

Here is my reasoning. My student loan interest rate is at 4.5%. That interest paid is also deducted on my taxes. The power of growth within my 401k and Roth is worth taking advantage of, and the earlier you do it the more powerful it is. Let's say the compounding growth is an average of 6%. My money is accomplishing more going into those accounts, than it is paying off those student loans (gaining 6% instead of losing 4.5%). I'd obviously try to pay this off as quick as possible, but I think funding both retirement accounts at their max potential is more important.

Thoughts? Let me know if you have an opinion.

Happy Hump Day.

Comments

Post a Comment